Why BFSI Cannot Afford to Ignore Customer Experience

Let’s be honest nobody remembers their bank balance, but everyone remembers the frustration of being put on hold for 30 minutes when trying to resolve a transaction issue. In the world of Banking, Financial Services, and Insurance (BFSI), a single bad customer experience can mean more than just one unhappy client it can mean lost trust, regulatory complaints, and even customers moving their money elsewhere.

Here’s the thing: financial services are not like retail. If a customer doesn’t like a shopping app, they delete it and move on. But if a customer doesn’t trust a bank, lender, or insurer, they may close accounts, stop payments, and influence others to avoid that institution. That’s why customer experience in BFSI is no longer a “nice-to-have” it’s a survival strategy.

And yet, many BFSI firms still rely on outdated communication methods, leaving customers frustrated with slow responses, confusing processes, and lack of personalization. The scary part? Competitors who adopt modern tools like WhatsApp Business API, RCS business messaging, SMS marketing for banks, chatbots, and secure digital onboarding are already winning customer loyalty.

So let’s break down how BFSI leaders can enhance customer experience, the best practices to follow, and some case studies proving why it works.

Why Customer Experience Matters More in BFSI

- Trust equals money. In BFSI, customer trust isn’t just about feeling good it’s the very foundation of deposits, investments, and policies.

- Switching costs are lower. With digital-first neo-banks and fintechs entering the market, customers don’t think twice before switching service providers.

- Regulations demand it. Slow complaint resolution or non-transparent onboarding can lead to heavy penalties under compliance laws.

Competition is unforgiving. If one bank offers instant policy updates via WhatsApp while another sends snail-mail letters, the choice is obvious.

Best Practices for Enhancing BFSI Customer Experience

1. Personalized Banking and Insurance Communication

Customers don’t want to be treated like “account numbers”they want relevant, personalized updates. Generic emails about “special offers” don’t cut it anymore.

- Use customer data smartly. For example, instead of sending a blanket SMS saying “We offer home loans,” send a personalized WhatsApp message saying, “Your pre-approved home loan of ₹25 lakhs is ready. Tap here to apply instantly.”

- Segment communications. Insurance policyholders need reminders about premium due dates. Mutual fund investors need updates on NAVs. Loan customers need EMI reminders. Personalization creates stickiness.

- Omnichannel presence. A customer might want loan updates via SMS, but claim settlement details on WhatsApp. Offering choice builds loyalty.

A leading Indian private bank rolled out personalized WhatsApp notifications for loan updates and credit card transactions. Result? Complaint calls dropped by 28%, and NPS (Net Promoter Score) went up.

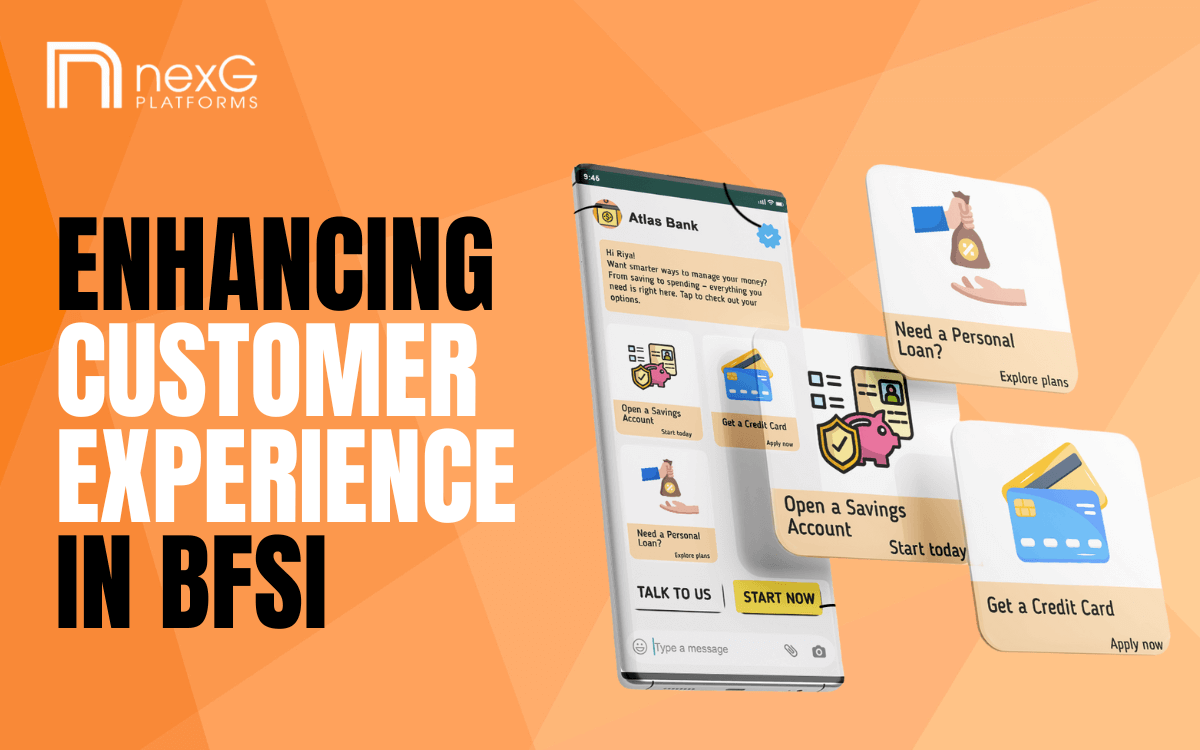

2. Instant Loan or Policy Updates via WhatsApp, RCS, and SMS

When it comes to money, delays cause anxiety. Customers hate logging into portals or waiting for emails just to check loan status or insurance policy details.

- WhatsApp Business API: Instant loan disbursal updates, credit card transaction alerts, claim settlement notifications all delivered where the customer already spends time.

- RCS Business Messaging: Rich messages that look like mini-apps inside SMS ideal for EMI reminders with one-click payment links.

- SMS Marketing for Banks: While old-school, SMS still has 98% open rates. Sending OTPs, fraud alerts, and payment confirmations via SMS keeps customers secure and informed.

Imagine a customer not getting a fraud alert in time because the bank relied on email. By the time they see it, their account is already drained. That’s how one weak communication channel can destroy decades of trust.

An insurance company started sending real-time claim updates via RCS and WhatsApp. Customers could track claims like food delivery orders. Claims resolution satisfaction went up by 40%.

3. Secure and Transparent Digital Onboarding

Onboarding is the first impression. A complicated, paper-heavy KYC process is enough to scare customers away.

- Digital KYC: Customers can upload documents directly through secure WhatsApp/RCS flows.

- Real-time verification: Chatbots guide users through ID uploads, selfies, and e-signatures.

- Transparent progress updates: Send customers instant updates at every stage “Your KYC is under review,” “Account activated successfully.”

If onboarding feels shady or confusing, customers assume the institution is unreliable. Worse, regulatory gaps in onboarding can result in penalties and reputational damage.

A mid-sized bank digitized its loan onboarding journey via chatbots. Customers got approvals in 24 hours instead of 7 days. New account sign-ups jumped by 60% in 3 months.

4. Chatbots for 24/7 Banking and Insurance Support

Customers expect instant answers. They won’t wait till 10 AM for the call center to open when they’re locked out of net banking at midnight.

- AI-powered chatbots handle FAQs like “What’s my account balance?” or “When is my premium due?” instantly.

- Escalation to human agents ensures sensitive cases (fraud, blocked cards) get real-time help.

- Multilingual support removes language barriers, especially in Tier-2 and Tier-3 cities.

Poor support = lost customers. Research shows that 60% of BFSI customers switch providers after just 2-3 bad service experiences.

A life insurance provider deployed a WhatsApp chatbot for policy servicing. Customers could update nominee details, download policy documents, and track claims all without human intervention. Support ticket volume dropped by 45%.

Common Pitfalls BFSI Firms Must Avoid

- Relying only on email. Customers don’t check email as often as WhatsApp or SMS.

- Using jargon. Financial terms confuse customers. Keep communication simple.

- Ignoring compliance. Personalized communication must also follow data privacy laws.

- Delaying responses. In BFSI, hours feel like days. Customers expect updates in real time.

Future Trends in BFSI Customer Experience

- Hyper-personalization with AI: Customers won’t just get “loan offers” they’ll get loan offers tailored to their spending patterns.

- Voice-based banking: IVR will evolve into smart voice assistants for financial transactions.

- Proactive communication: Instead of waiting for customers to ask, banks will notify them about potential fraud or missed EMI risks in advance.

- Unified omnichannel journeys: Customers won’t care if they use WhatsApp, SMS, or email they’ll expect the same experience everywhere.

The Risk of Doing Nothing

Here’s the scary truth: customers no longer compare their bank to another bank. They compare their bank to Amazon’s speed, Swiggy’s real-time updates, and Netflix’s personalization. If BFSI companies don’t adapt, they’ll lose to competitors who do.

The question is are you going to wait until frustrated customers leave, or are you ready to transform your communication today?

That’s where nexG Platforms comes in. By offering WhatsApp Business API, RCS business messaging, SMS marketing, voice solutions, and chatbot integrations, nexG helps BFSI leaders modernize customer journeys securely, transparently, and at scale.

Because in BFSI, trust isn’t built by slogans it’s built by every message, every update, and every interaction.